Tax Lessons Learned From Tesla

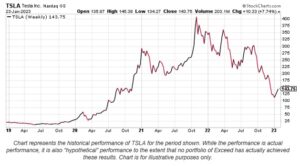

The past few years for Tesla (Ticker: TSLA) have been anything but mundane. Shares of the equity experienced a meteoric rise from mid-2019 to late 2022, with a trough-to-peak rally of over 3400% in a little over three years. However, after its parabolic ascent the shares declined by about 75% in a little over a year.

Opinions on the company are as polarizing as they come – some believe that it’s a cash-burning vortex destined for bankruptcy, while others are convinced Elon Musk can walk on water and TSLA is set to take over the world. Musk’s recent Twitter fiasco removed a lot of the sparkle from his image, and that shift in sentiment can be seen in Tesla’s recent performance. There was always an embedded “Elon premium” in the shares, as believers shunned fundamentals because of the CEO’s rockstar image. Is it possible that there is now an “Elon discount?”

Early investors in the company experienced a financial windfall between mid-2019 and November 2021, but many were likely caught up in the hype, which would limit a potentially prudent taking of some profit. Aside from human emotions, the most likely reason that a buy-and-hold investor refused to reduce their TSLA position after its rapid rise was the associated tax liability with selling shares. Let’s look at a hypothetical situation involving an early investment in TSLA…

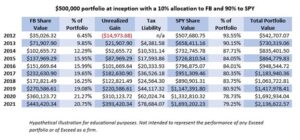

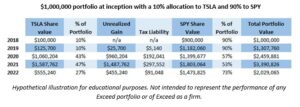

Assume a buy-and-hold investor with a $1M portfolio invested 10% of their capital in TSLA shares at an average price of $20 (split adjusted for today’s prices) at the end of 2018, and the remaining 90% of their capital was invested in a diversified market fund. For simplicity’s sake, in this example we’ll use the SPDR S&P 500 ETF trust (symbol SPY), an exchange traded fund (ETF) that aims to track performance of the S&P 500 index. So, on 1/2/2019 this hypothetical portfolio consisted of $100,000 in TSLA shares and $900,000 in SPY shares. The table below shows the performance of the Tesla and SPY positions, using end-of-year values. This illustration also assumes a 20% capital gains tax rate.

As you can see the Tesla position quickly grew into a substantial percentage of the total portfolio holdings. From the investor’s perspective, this is obviously a very good thing because it means that the TSLA position was appreciating rapidly. However, this rapid appreciation creates other problems associated with buy-and-hold investing. Multiple studies have shown that holding a concentrated portfolio generally leads to underperformance. 1Nathan Sosner, “When Fortune Doesn’t Favor the Bold. Perils of Volatility for Wealth Growth and Preservation. ”The Journal of Wealth Management Winter 2022, jwm.2022.1.189; DOI: https://doi.org/10.3905/jwm.2022.1.189 2Bernt Arne Ødegard, “The diversification cost of large, concentrated equity stakes. How big is it? Is it justified?” Finance Research Letters Volume 6, Issue 2. https://doi.org/10.1016/j.frl.2009.01.003 3Baird’s Private Wealth Management Research, “The Hidden Cost of Holding a Concentrated Position. Why diversification can help to protect wealth.” https://www.bairdwealth.com/siteassets/pdfs/hidden-cost-holding-concentrated-position.pdf

In addition to the heavy concentration risk, the total portfolio volatility grew substantially. TSLA has a five-year monthly beta of 2.03, meaning that it’s more than twice as volatile as “The market.” As a result, total portfolio volatility grew by nearly 50 percent over the first three years. Elevated levels of volatility that lead to underperformance can be detrimental to risk-adjusted performance metrics like Sharpe and Sortino Ratios.

It’s easy to look back and wonder why an investor didn’t rebalance their portfolio after such a gigantic move higher by TSLA, but hindsight is always 20/20. At its peak at the end of 2021, the theoretical tax liability associated with the TSLA holding was approximately three times the initial investment amount, and nearly 30% of the initial portfolio value! Upon the liquidation of shares, this tax liability can be seen as an immediate loss of portfolio value.

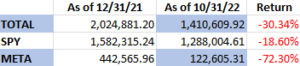

Rapid ascents by companies like this aren’t anything new. History is littered with similar examples of companies that quickly rose to prominence, only to fall back to earth. A few that immediately come to mind are Yahoo, Dell Computer, Zoom, Meta, Netflix, Nokia, and Blockbuster Video. Generally speaking, companies that rise the most during bull markets may depreciate rapidly during market downturns. It’s imperative that investors harvest gains and periodically rebalance their portfolios in order to avoid substantial drawdowns.

The good news is that there are solutions to these common problems. Options are often (and rightly) viewed in a negative light among retail investors, as they can be very risky and lead to substantial losses. Options are complex and can be intimidating to even the most seasoned investor. What many people don’t realize, though, is that options can also be powerful tools for tax optimization and hedging within a portfolio. When correctly implemented, an option overlay strategy may completely eliminate tax liability on certain concentrated positions, while simultaneously hedging downside risk. There are of course transaction costs involved, as well as advisory fees in the case of an overlay strategy, but the ability to exit these positions tax neutrally while also reducing portfolio volatility can have a substantial positive effect on long-term capital appreciation.

If you or a client are dealing with how best to address the tax liability and downside risk concerns that often accompany concentrated positions, feel free to reach out to the team at Exceed Investments. Members of Exceed’s Portfolio Management Team have over 38 years of professional options experience and are well-versed in the tax code. These strategies can be tailored to fit specific investment goals and satisfy immediate needs. When executed properly, these option overlay strategies may reduce or eliminate tax liability, lower risk, and help you and your clients achieve their financial goals in an efficient manner.

Contact us for a consultation.

This blog post is for informational or educational purposes only and is not intended as investment advice. Any discussion of investment strategy or approach is intended only to illustrate investment concepts and in no case does the discussion represent Exceed Advisory’s investment performance or the results of any Exceed Advisory portfolio. We provide investment advice only to clients and only after entering into an advisory agreement and obtaining information concerning individual needs and objectives. We think the information provided is accurate, but accuracy is not guaranteed. All investing in securities involves risks, including the risk of loss.