Common Misconceptions About Option Strategies: What Advisors Need to Know

Options can be a powerful tool for financial advisors looking to enhance client returns, manage risk, and potentially exit a concentrated position in a tax-efficient manner. However, many advisors hesitate to incorporate options due to widespread misconceptions. In this article, we’ll debunk some of the most common myths about option strategies and provide insights into how advisors can effectively leverage them for their clients.

Misconception #1: Selling Options is Too Risky

One of the most persistent myths is that selling options is inherently dangerous. While certain strategies—such as selling naked calls—carry significant risk, selling options strategically against equity holdings can enhance portfolio returns while maintaining controlled risk exposure. Strategies such as covered calls and cash-secured puts allow advisors to generate consistent income while maintaining defined risk limits. The key is understanding the risks and structuring trades appropriately to align with investment objectives.

Misconception #2: Options Are Only for Speculators

Many advisors assume that options are tools meant only for aggressive traders looking to make quick profits. While this may be true with regard to speculatively buying options, option-selling programs can play a crucial role in conservative portfolio management. Advisors can use option overlays to generate additional income through covered call strategies or sell puts to enter stock positions at more favorable prices. When used correctly, selling options can provide an additional layer of risk management rather than being purely speculative.

Misconception #3: Options Are Too Complex for Clients to Understand

It’s true that options involve additional layers of complexity compared to traditional stock investing. However, that doesn’t mean they are incomprehensible or unusable. Many advisors successfully incorporate option-selling strategies by educating clients on their benefits and risks in a straightforward manner. Explaining how a covered call generates additional income makes these concepts more digestible for clients. Clear communication and proper risk management help bridge the knowledge gap and make more options accessible. Advisors who don’t have the requisite knowledge or time required to implement these strategies can hire an outside expert like Exceed.

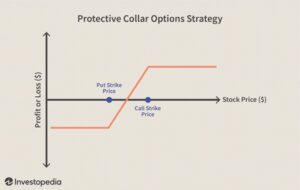

Misconception #4: Selling Options is a High-Volatility Strategy

While strategies such as covered calls or collars can be very beneficial in volatile markets, selling options is not solely a high-risk, high-volatility play. Even in low-volatility environments, selling options can provide ongoing income and improve portfolio efficiency. Covered call strategies work best when markets are flat or slowly rising, but they can also be profitable in strong bull markets. By structuring trades correctly, advisors can benefit from different market conditions, not just volatile ones.

Misconception #5: Options Are Too Expensive to Implement

Some advisors believe that options are costly due to margin requirements or potential losses. However, many option-selling strategies involve well-defined risks that can be managed with proper portfolio allocation. Covered calls, for example, do not require additional capital beyond owning the underlying stock, and cash-secured puts ensure that sufficient cash is available to buy the underlying stock if assigned. With low-cost option trading now widely available, cost barriers are lower than ever.

Final Thoughts

Misconceptions about options have led many financial advisors to overlook their potential benefits. However, when used strategically, selling options can be a valuable tool for generating income, managing risk, and enhancing tax efficiency. By debunking these common myths and educating both themselves and their clients, advisors can take full advantage of what option-selling strategies have to offer. Instead of viewing options as overly risky or complex, advisors should see them as a flexible instrument that, when properly implemented, can improve client outcomes and portfolio resilience.

IMPORTANT DISCLOSURE: The information in this blog is intended to be educational and does not constitute investment advice. Exceed Advisory offers investment advice only after entering into an advisory agreement and only after obtaining detailed information about the client’s individual needs and objectives. No strategy can prevent all losses or guarantee positive returns. Options trading involves risk and does not guarantee any specific return or provide a guarantee against all loss. Clients must be approved for options trading at the custodian holding their assets, and not all retirement accounts are permitted to trade options. Transaction costs and advisory fees apply to all solutions implemented through Exceed and will reduce returns.