Where Are Those “Top 10” Companies Now? – “Millennium” Focus

“Top” companies can seemingly do no wrong during their ascent. Whether filtered by top US companies by market cap or fastest growing over the last decade, these companies tend to be household names with a ton of caché. Right now, the top US company by market cap is Apple (AAPL). The fastest growing for the last decade (2010s) is Netflix (NFLX). Some of the luster has already caught up to Netflix as competitors have filled the gap. Apple, though, still seems to dominate. Will that be the case in five years? 10 years? When a fifty-something is ready to retire and dip into their nest-egg?

The only sure thing in investing is uncertainty, but maybe we can learn something from history. How have the “Apples” and “Netflixes” of the past performed over time? Today, let’s look back to 2000 and see if there are any important lessons for investors.

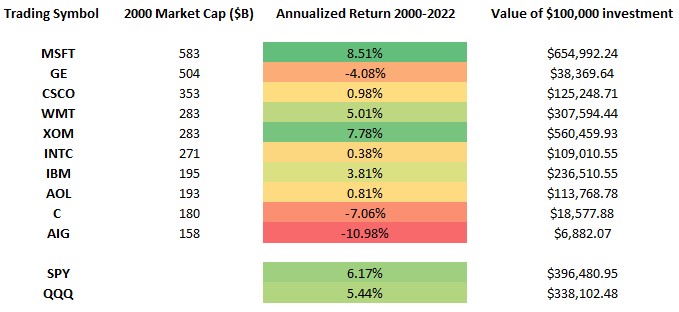

Below is a list of the ten largest companies by market capitalization as of the start of 20001As of the close of trading on 12/31/1999, and their performance since. These return numbers include dividend reinvestment and consider a hypothetical $100,000 investment in each security on the close of trading for 19992As of the close of trading on 12/31/1999. The ending value is as of 12/31/2022. We’ve also provided information on the results of the SPDR S&P 500 ETF Trust (SPY), representing large-cap US equities, and the Invesco QQQ Trust (QQQ), an ETF with holdings of mostly large-cap stocks from the Nasdaq 100, during the same period. While it’s not possible to invest directly in an index, index returns are widely used to reflect the performance of “markets” overall.

The hypothetical performance shown in the table above is for illustrative purposes only and is not intended to represent the performance of any Exceed Advisory portfolio or of Exceed as a firm.

This decade was an especially difficult time in markets, as the tech bubble burst in 2000 and led to a catastrophic selloff in equities over the next two years. Markets recovered and recouped most of the losses from the tech bubble over the subsequent five years, but that rally led right into the financial crisis of 2008. Stocks fell precipitously once again before bottoming in early 2009, but this period was essentially a lost decade for investors. It’s evident from the table above that this era of investing was fraught with risk, as even the most established companies weren’t insulated from the crisis. Of the 10 largest companies by market capitalization in 2000, only investments in MSFT and XOM would’ve yielded returns in excess of market indices. Of the other 8 companies on this list that underperformed the broad market, only two generated dollar returns of at least half of that of a similar investment in SPY. Investments in three of these companies (AIG, C, and GE) would’ve resulted in significant capital losses over this twenty-two-year period. Market crises create the potential for big losses in individual names, and this period was no exception. It’s especially important to have a diversified portfolio during such times, and history will likely repeat itself in the future on a long enough timeframe.

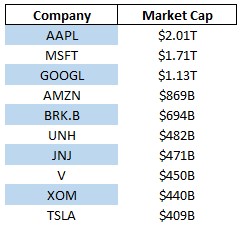

Below is the current list of the ten largest U.S. corporations. We will continue to look at different slices of time in future blogs as we did above, but the theme remains consistent – historically, most of the biggest companies have underperformed the broad market over long periods of time. It seems unfathomable that any of these companies could be poor investments going forward, but history suggests otherwise. That said, it’s also true that past performance isn’t a guarantee of future results, so we don’t know for sure what the future will bring. We do, though, think caution is warranted when assuming that today’s top performers will continue to be tomorrow’s top performers.

The solution to combat a concentrated portfolio of mega-cap stocks is simply to reduce position sizes and rebalance into a diversified market portfolio. Multiple studies have shown that concentrated portfolios often underperform over long time periods, and the optimal portfolio decision is to rebalance and reduce volatility and exposure.3Nathan Sosner, “When Fortune Doesn’t Favor the Bold. Perils of Volatility for Wealth Growth and Preservation. The Journal of Wealth Management Winter 2022, jwm.2022.1.189; https://doi.org/10.3905/jwm.2022.1.189 4Bernt Arne Ødegard, “The diversification cost of large, concentrated equity stakes. How big is it? Is it justified?” Finance Research Letters Volume 6, Issue 2. https://doi.org/10.1016/j.frl.2009.01.003 5Baird’s Private Wealth Management Research, “The Hidden Cost of Holding a Concentrated Position. Why diversification can help to protect wealth.” https://www.bairdwealth.com/siteassets/pdfs/hidden-cost-holding-concentrated-position.pdf If you or your clients have concentrated positions in any of the above companies, Exceed Investments can help. Exceed’s tools can be implemented to hedge large investments, and in many cases reduce them to a desired level, often without having to pay capital gains tax. There are of course transaction costs involved, as well as advisory fees in the case of an options strategy, but the ability to exit these positions tax neutrally while also reducing portfolio volatility can have a substantial effect on long-term capital appreciation.

Contact us for a consultation.

IMPORTANT DISCLOSURE: The information in this blog is intended to be educational and does not constitute investment advice. Exceed Advisory offers investment advice only after entering into an advisory agreement and only after obtaining detailed information about the client’s individual needs and objectives. Hedging does not prevent all losses or guarantee positive returns. Transaction costs and advisory fees apply to all solutions implemented through Exceed.